_edited_.png)

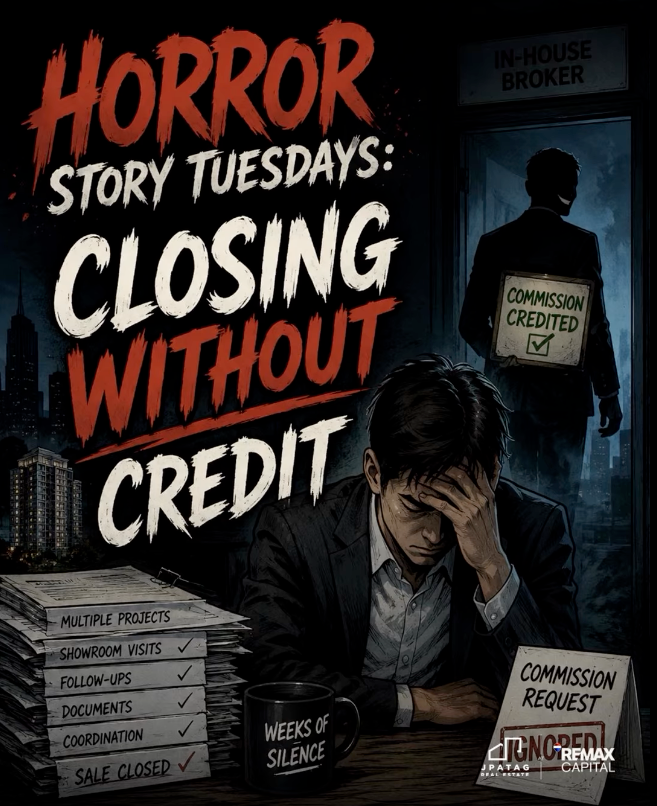

CLOSING WITHOUT CREDIT

- Jun 8

- 1 min read

Once upon a time, a broker had a client looking for a pre-selling condo unit.

The broker spent weeks searching for options.

He shortlisted multiple projects, coordinated showroom visits, compared layouts, discussed payment terms, analyzed locations, and patiently walked the client through the pros and cons of each property.

Some projects were too expensive. Some had poor layouts. Others simply didn’t feel right for the client.

After several viewings and follow-ups, the broker finally found a project in a CBD that the client genuinely liked.

The broker arranged another showroom visit, answered concerns, coordinated with the sales team, and continued assisting the client until the buyer finally decided to proceed with the purchase.

But the work didn’t stop there.

The broker then guided the client through the reservation process, collected the required documents, coordinated submissions, and helped complete everything needed to close the sale.

Transaction completed.

Naturally, the broker then followed up for the commission.

Weeks passed. Silence.

After another follow-up, the developer finally responded: the commission would instead be credited to one of their in-house brokers because the buyer supposedly turned out to be an “existing client” of that in-house broker.

In other words, after the external broker did the searching, the presentations, the follow-ups, the convincing, and the paperwork, someone else suddenly appeared at the finish line.

To be fair, not all developers operate this way. Many developers still protect broker relationships and honor professional ethics.

But stories like this are exactly why brokers eventually become selective about which developers they choose to work with.